ML for Markets (AI Scholars)

Combining machine learning with stock-market analysis and trading.

PI / Advisor: Dr. Catia Silva

Institution / Department: University of Florida, Department of Electrical and Computer Engineering

Timeframe: August 2025–present (Expected Completion May 2026)

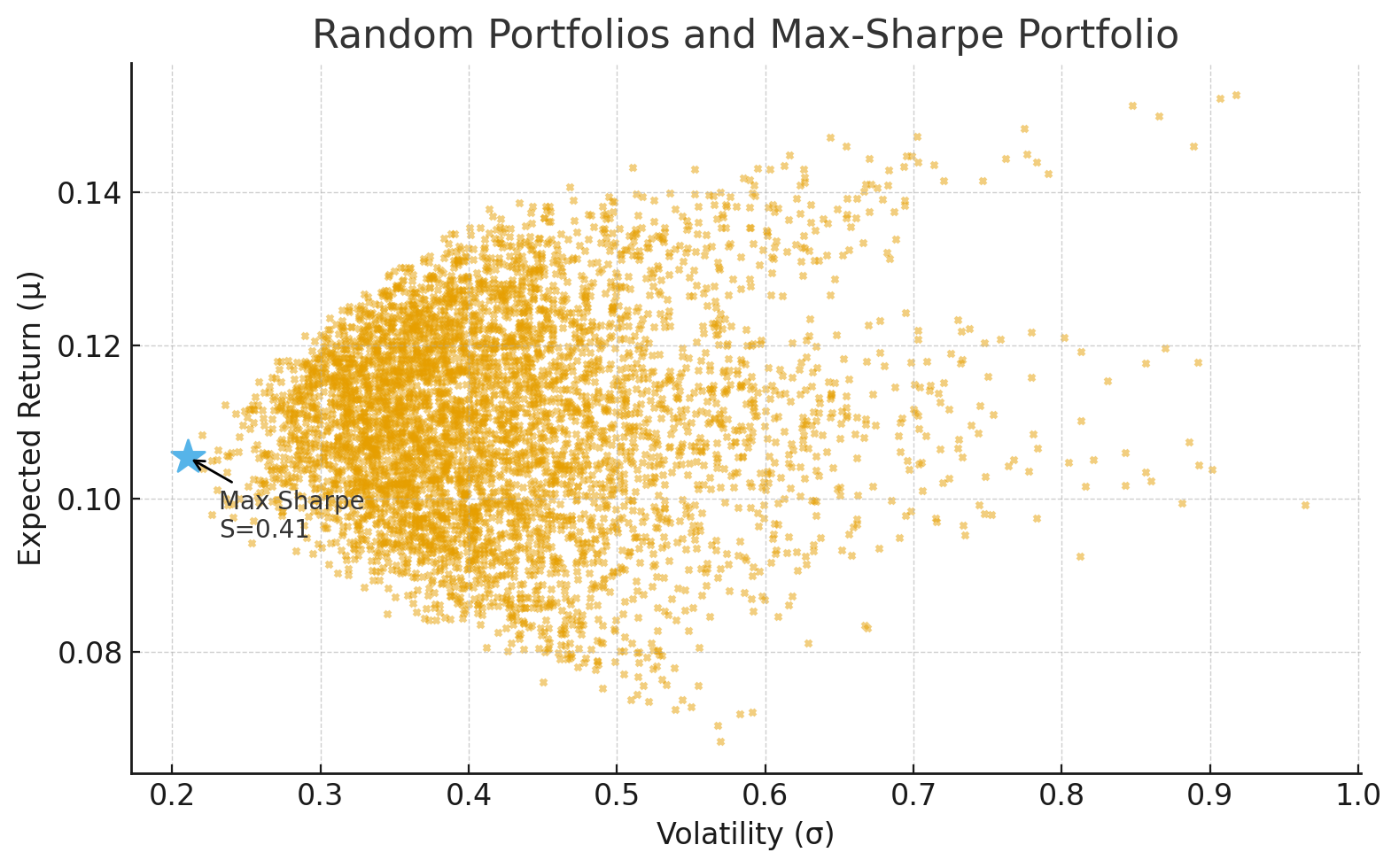

Research Focus

This project, conducted through UF’s AI Scholars Program, explores the use of machine learning techniques to analyze financial markets and inform trading decisions. The work is focused on balancing predictive performance with interpretability, aiming to highlight both the potential and limitations of ML in high-variance domains like finance.

Responsibilities

I am currently designing the experimental framework, identifying baseline models, and surveying literature on ML in finance. The project is in its early stages, and as it develops, I will refine methods, evaluate algorithms, and present findings.